REFINANCE BROKER KILMORE & REGIONAL VICTORIA

REFINANCE,

RESTRUCTURE

OR REVIEW?

Thinking about refinancing your home loan? Mortgage Muster helps homeowners compare refinance options, review repayments, access equity and explore debt consolidation or other finance paths where suitable.

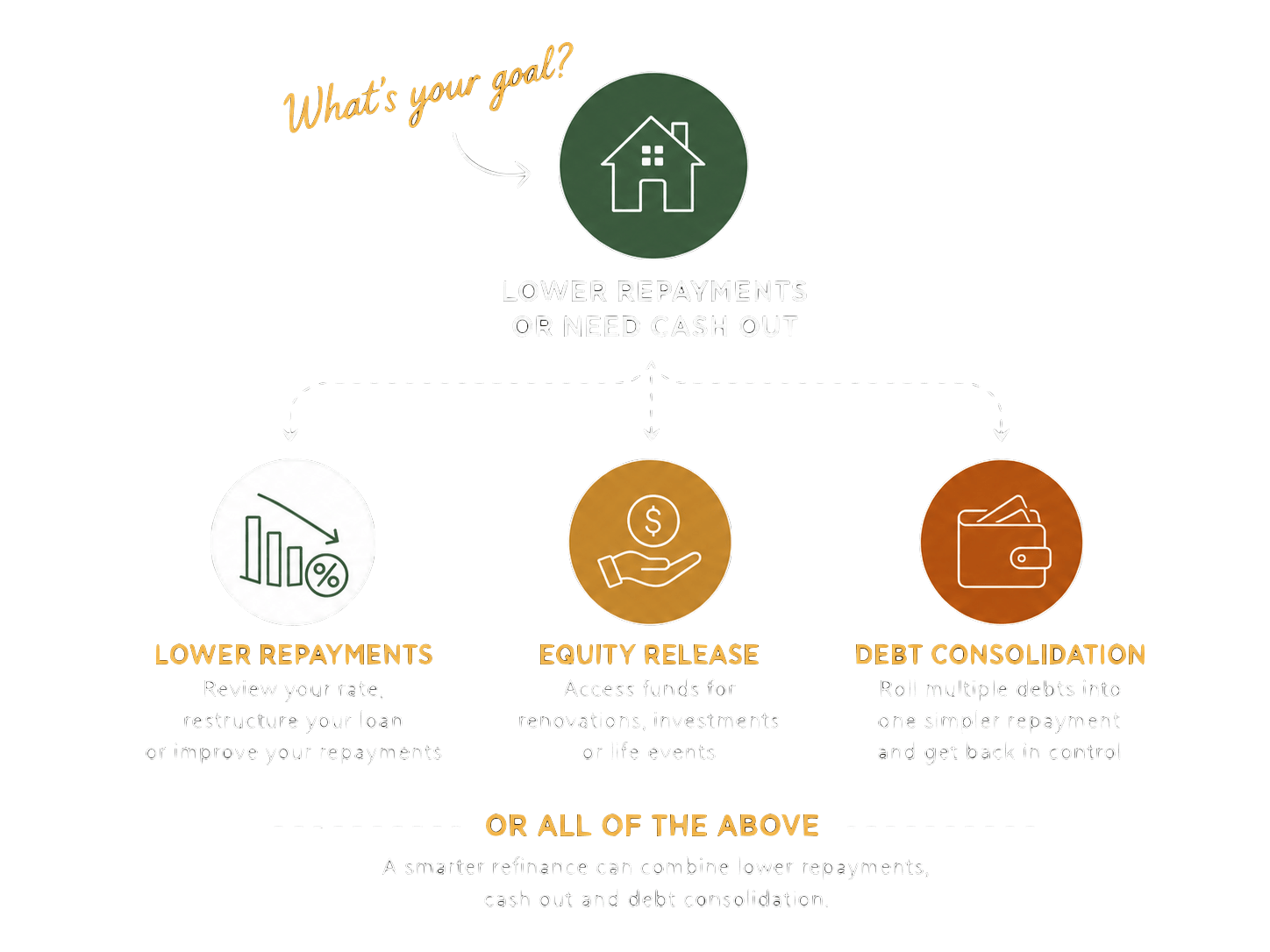

Could refinancing help with more than your rate?

A refinance is not always just about chasing a lower interest rate. Depending on your equity, income, lender policy and goals, it may help reduce pressure, tidy up debts, access funds or make your loan work better for where life is heading.

Repayments too high?

We’ll review your current rate, repayments and loan structure to see whether refinancing could put you in a better position.

Want to tidy up debts?

Personal loans, car loans and credit cards can get messy. We’ll help you compare whether debt consolidation makes sense.

Need funds for home Upgrades?

Planning a kitchen, driveway, landscaping, shed or renovation? We can look at whether accessing equity may be suitable.

Business or work needs?

Self-employed or running a business?

Depending on your position, refinancing may help with work vehicles, equipment, cash flow or business debt where suitable.

Not sure which option fits?

That’s exactly what the first chat is for.

Any information on this website is of a general nature only and does not take into account your objectives, financial situation or needs.

You should consider whether the information is appropriate to your circumstances before making any decisions. We recommend obtaining independent legal, financial, and tax advice where necessary.

The Mortgage Muster

Difference

FINANCE GUIDANCE THAT LOOKS

Beyond the loan

We take the time to understand your home, business, income, assets and goals, then talk you through practical lending options in plain English.

✓ Straight talk, no jargon

✓ Lending options that fit the full picture

✓ Ongoing support after settlement

Refinance Faq

-

Refinancing may help reduce costs in a few different ways, depending on your situation. We review your current home loan, then compare it against other lending options to see whether a lower rate, sharper structure or better loan setup may be available.

Sometimes the benefit comes from a lower rate. Sometimes it comes from restructuring the loan, changing features, consolidating debts or reducing repayments in the short term. The key is making sure the new loan suits your goals, not just chasing a headline rate.

-

Personal loans and credit cards are often unsecured, which often mean higher interest rates. Car loans may have fixed terms, balloons or repayments that no longer fit your cash flow.

In some cases, consolidating debts into your home loan may help reduce monthly repayments, simplify your finances and reduce multiple fees. It can also spread the debt over a longer loan term, which may lower repayments, but it can increase the total interest paid over time.

We’ll help you understand the trade-off before you decide. -

Cash out means using available equity in your property and turning part of that “paper value” into usable funds. This may be used for things like renovations, a new kitchen, landscaping, solar panels & batteries, a driveway, a shed, education costs, a holiday or other personal goals.

It is still borrowed money, so we’ll help you look at the purpose, loan structure, repayments and long-term impact before recommending whether cash out is suitable. -

Sometimes, but it is very lender specific. Depending on your income, equity, lender policy and the purpose of the funds, some lenders may allow refinancing to help with business debt, work vehicles, equipment, cash flow or other self-employed needs.

This is where it helps to work with someone who understands both mortgage lending and asset finance.

A full home loan refinance may be suitable, or a separate asset, vehicle or business finance option may make more sense. We’ll talk through the options and help you work out what fits.

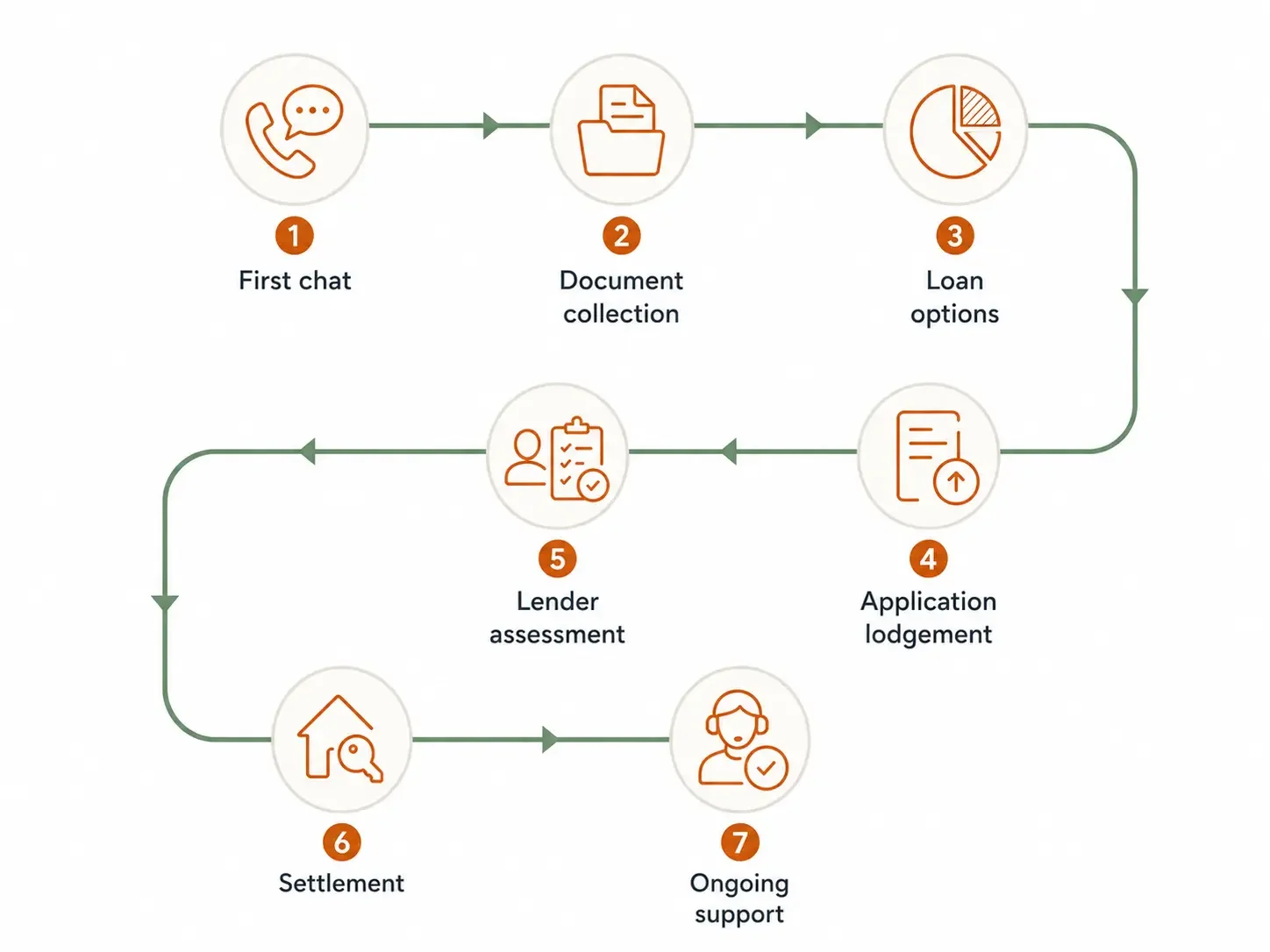

How it Works

A simple 7-step Process