SELF-EMPLOYED MORTGAGE BROKER KILMORE & REGIONAL VICTORIA

Self-employed lending

without the runaround

Getting a home loan when you’re self-employed can feel harder than it should. Mortgage Muster specialises in helping business owners, sole traders, contractors and company directors work through income, documents and lender options, including full doc and alt doc lending where suitable.

Self-employed lending needs more than a quick calculator.

We take the time to understand how your income is earned, how your business is structured and what you’re trying to achieve. Sometimes the answer is a home loan. Sometimes it may be asset finance, equipment finance or a business lending option that keeps things cleaner.

Sole trader or contractor?

Your income might not fit neatly into a payslip. We’ll help review your tax returns, ABN history and income pattern to see which lenders may suit.

Need an

alt doc option?

Some lenders may consider BAS, business bank statements or accountant declarations when tax returns don’t show the full story.

Not sure which option fits?

That’s exactly what the first chat is for.

Company or trust

income?

If your income flows through a company, trust or family business, lender treatment can vary. We’ll help unpack the structure and explain what may be usable.

Need equipment finance?

Need a ute, trailer, machinery or tools for the business?

We can look at asset finance, business lending or home loan options where suitable.

Any information on this website is of a general nature only and does not take into account your objectives, financial situation or needs.

You should consider whether the information is appropriate to your circumstances before making any decisions. We recommend obtaining independent legal, financial, and tax advice where necessary.

The Mortgage Muster

Difference

FINANCE GUIDANCE THAT LOOKS

Beyond the loan

We take the time to understand your home, business, income, assets and goals, then talk you through practical lending options in plain English.

✓ Straight talk, no jargon

✓ Lending options that fit the full picture

✓ Ongoing support after settlement

Self Employed Loan Faq

-

es, many self-employed borrowers can get a home loan, but the right lender and document requirements matter. Lenders usually want to understand your income, business history, tax returns, debts and whether the income is stable enough to support the loan.

At Mortgage Muster, we help sole traders, contractors, company directors and business owners work through the numbers and compare lender options that may better suit their situation.

-

It depends on the lender and the type of loan. Common documents can include personal and business tax returns, financial statements, notices of assessment, business bank statements, BAS statements, accountant letters and details of your business structure.

Some clients fit a full-doc application. Others may need to explore alt-doc options, where suitable. We’ll help you understand what each lender is likely to need before you apply.

-

Alt doc lending is where a lender may consider alternative income documents instead of relying only on full tax returns and financial statements. This may include BAS, business bank statements, accountant declarations or other documents accepted under that lender’s policy.

It does not mean “no documents”. It means your income may be assessed using different evidence, which can help when your tax returns do not clearly show your current trading position.

-

Yes, self-employed clients often need finance for utes, trailers, tools, machinery, equipment or other business assets. Depending on your situation, this may be handled through asset finance, equipment finance, business lending or, in some cases, broader home loan planning.

Because Mortgage Muster works across both mortgage and asset finance, we can talk through the bigger picture and help you consider which structure may fit your goals, cash flow and lender requirements.

Prefer to Talk it Through?

Give us a buzz

0492 990 723

Drop us a line

gday@mortgagemuster.com.au

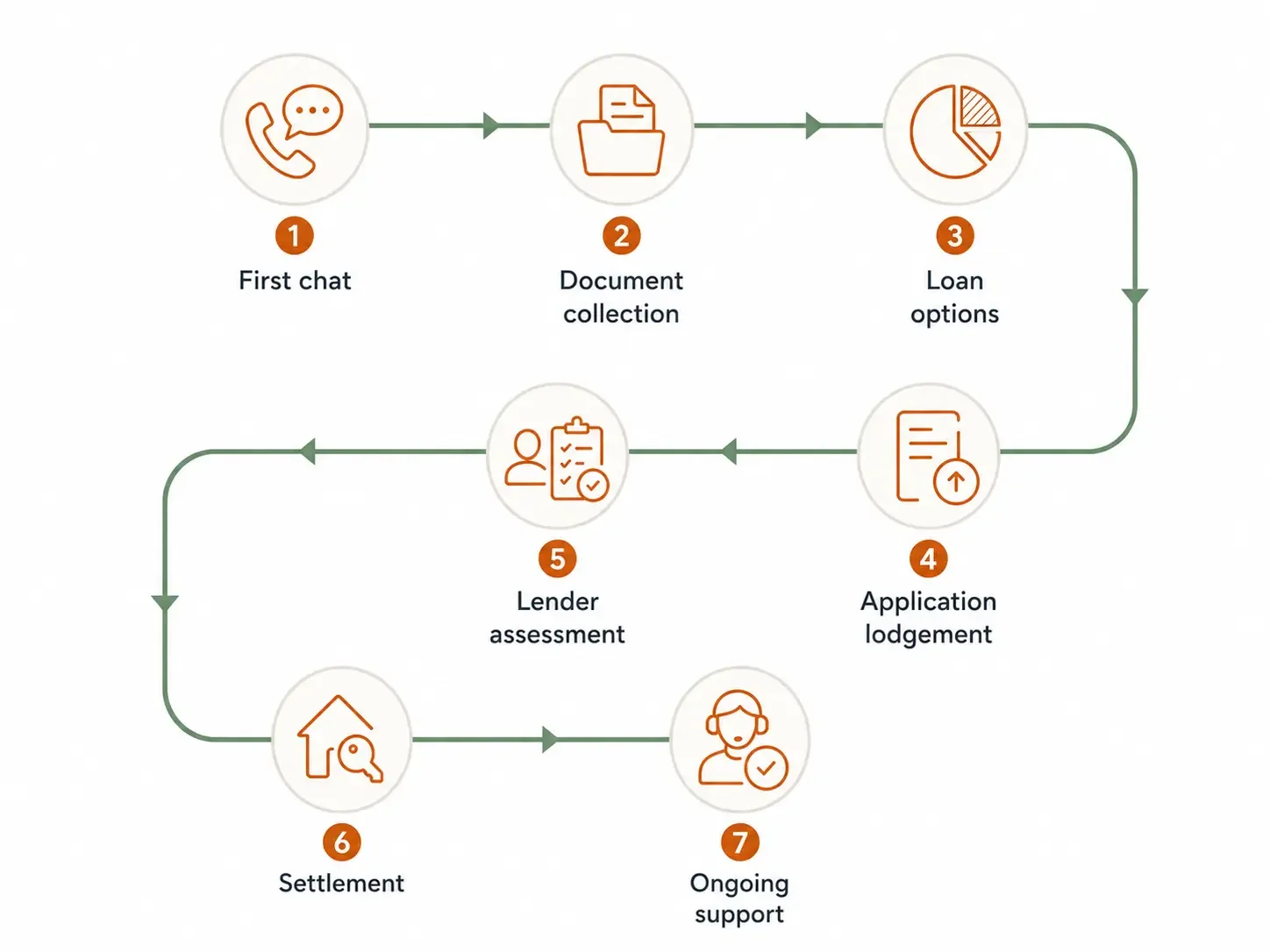

How it Works

A simple 7-step Process